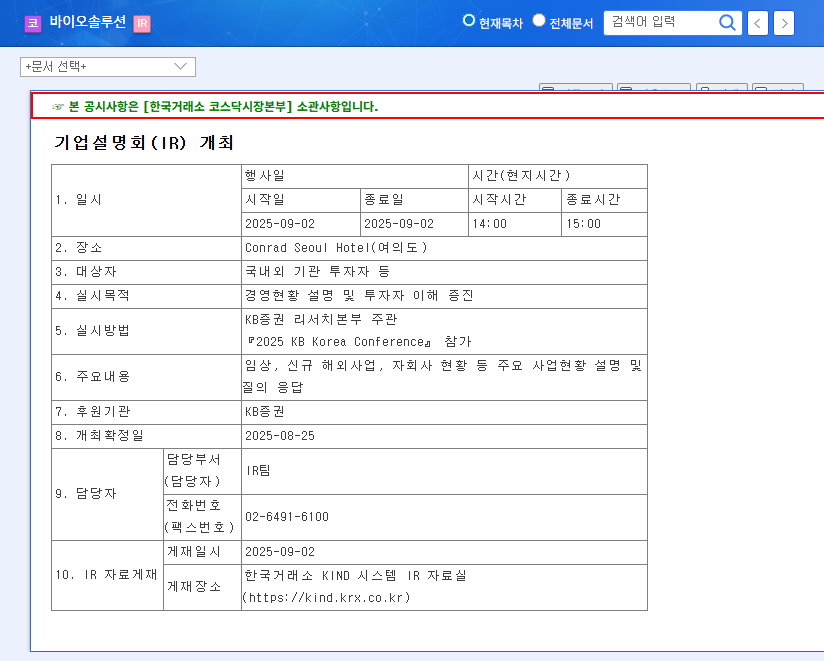

Biosolution IR: What to Expect?

During the IR, Biosolution’s management team will provide updates on clinical trials, new overseas business plans, and subsidiary performance, while also addressing investor questions. The market is particularly interested in updates on CARTyLIFE’s US FDA RMAT designation and global Phase 2 clinical trial results, as well as details on the new animal testing alternative business.

How Will the IR Impact the Stock Price?

Positive Factors:

- Progress in CARTyLIFE’s overseas clinical trials and commercialization

- Growth potential of new business areas

- Increased transparency through direct communication with management

Negative Factors:

- High debt-to-equity ratio and continued losses

- Past sanctions history

- Potential for unmet market expectations

Key Considerations for Investors

Investors should carefully analyze the information presented at the IR to assess the company’s true growth potential and financial soundness. Pay close attention to the following:

- Clinical trial results and commercialization strategies for each pipeline

- Financial soundness improvement plan

- Competitiveness and monetization strategy of new businesses

By considering the IR presentation and management’s responses, investors can assess the company’s future growth prospects and make informed investment decisions.

Frequently Asked Questions

What are Biosolution’s main businesses?

Biosolution operates in cell therapy (CARTyLIFE, CARTyROID), human stem cell-derived materials, human tissue models, animal pharmaceuticals, and non-clinical evaluation platforms.

What are the key takeaways from this IR?

The main focus will be on updates regarding CARTyLIFE’s overseas clinical trials and commercialization progress, growth strategies for new businesses (like animal testing alternatives), and plans for improving financial health.

What should investors be cautious about?

Investors should consider the company’s high debt-to-equity ratio, continued losses, and past sanctions history before making any investment decisions.