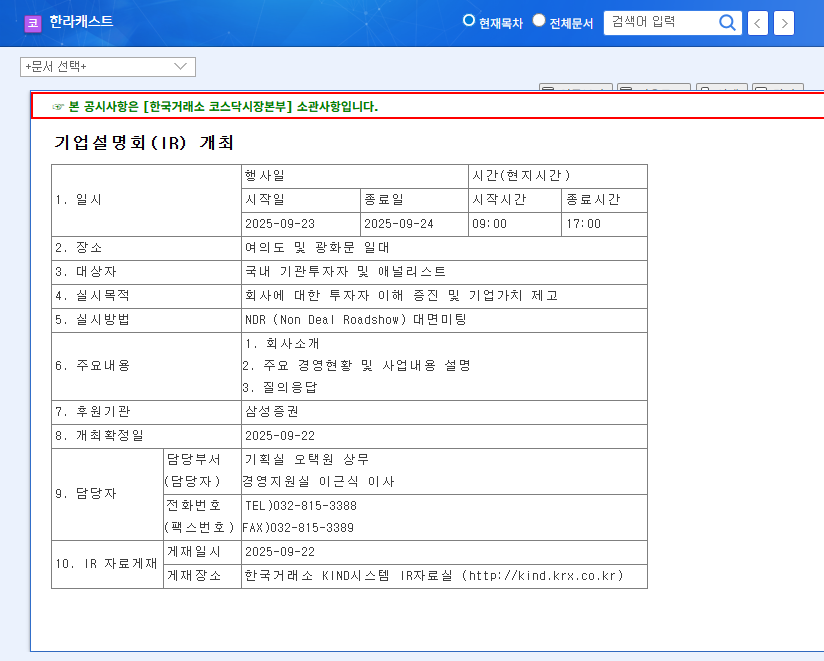

HanlaCast IR Key Analysis: What’s Happening?

HanlaCast will hold an investor relations (IR) presentation on September 23, 2025, to present its future vision and growth strategy to investors. They are expected to disclose specific business plans for new growth drivers such as future mobility, robotics, and secondary batteries, as well as their post-IPO fund utilization plan.

IR Background and Importance: Why Does it Matter?

Recently listed on KOSDAQ, HanlaCast faces the challenge of demonstrating its future growth potential amidst high investor expectations. This IR presents a crucial opportunity to convincingly convey their growth story and build investor confidence. Presenting a concrete roadmap for future mobility, robotics, and secondary battery businesses, and demonstrating financial stability will be key aspects of this IR.

IR Positive & Negative Scenarios: What Outcomes Can We Expect?

- Positive Scenario: Presentation of concrete achievements and future strategies expected to lead to stock price increase and investor inflow.

- Negative Scenario: Business uncertainty and insufficient resolution of financial risks could lead to stock price decline and dampened investor sentiment.

Action Plan for Investors: What Should You Do?

Investors should carefully analyze the IR content to inform their investment decisions. Key areas to examine include the actual competitiveness of the future mobility, robotics, and secondary battery businesses, financial soundness plans, and fund utilization strategies. Flexibility in adjusting investment strategies based on market reactions and expert analysis following the IR is also essential.

Frequently Asked Questions

What are HanlaCast’s main businesses?

HanlaCast is a precision parts manufacturer supplying components to various industries, including mobile, home appliances, automotive, and robotics. Future mobility, robotics, and secondary batteries are their key growth drivers.

What are the key takeaways from the HanlaCast IR?

The key takeaways include a concrete roadmap for future mobility, robotics, and secondary battery businesses, strategies for ensuring profitability of the order backlog, and financial risk management plans.

What precautions should investors take when considering HanlaCast?

Investors should consider factors such as high financial costs, raw material price volatility, and whether the company meets market expectations post-IPO. Carefully analyzing the IR content and market reactions is crucial for making informed investment decisions.