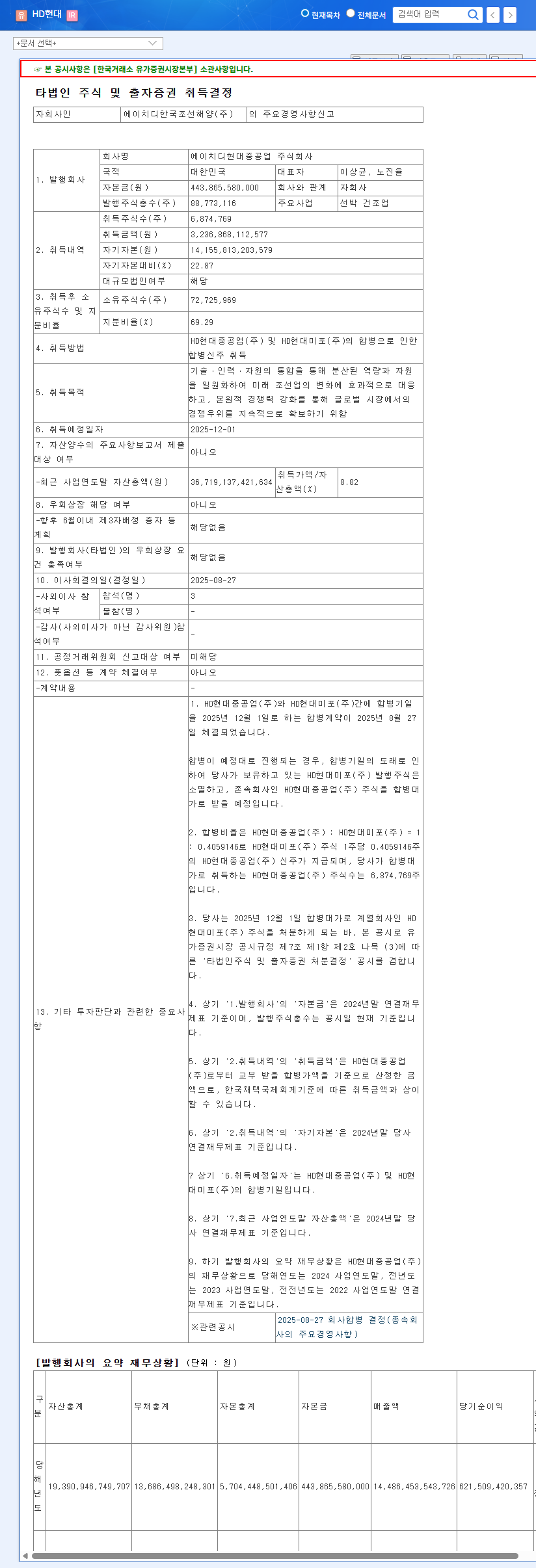

1. What’s Happening at LG H&H?

The Background and Current Status of the Divestment Rumors

LG H&H is exploring various options, including the potential sale of its beverage subsidiary, to enhance business competitiveness and management efficiency. While the company denied rumors about selling Coca-Cola Beverage, concerns about the sluggish performance of the beverage business remain.

2. Why the Restructuring?

Fundamental Analysis and Financial Health Check

Despite growth in luxury brands within its beauty business, LG H&H faces challenges due to uncertainties in the Chinese market and intensifying competition in the domestic market. While the HDB business remains stable, the beverage business is grappling with slow growth and volatile raw material costs. Since 2022, revenue and operating profit have been declining, and ROE is also projected to fall. In this context, restructuring appears to be an inevitable choice.

3. What’s Next?

Potential Impacts and Risks of the Restructuring

- Potential Positives: Streamlined business structure, improved profitability, new growth engines, enhanced shareholder value

- Potential Negatives: Short-term uncertainty, sale price and conditions, intensified competition, lower market expectations, fluctuations in exchange rates and raw material prices

Restructuring presents both opportunities and risks. Successful restructuring hinges on factors such as negotiation of sale conditions, new business investment strategies, and risk management.

4. What Should Investors Do?

Investment Strategy and Key Monitoring Points

The current investment outlook for LG H&H is ‘Neutral’. Investors should closely monitor the details of the restructuring plan, the performance of the beauty and HDB businesses, and fluctuations in exchange rates and raw material prices. The success of securing funds through the sale of the beverage subsidiary and securing new growth engines will be crucial investment decision points.

FAQ

Is the sale of LG H&H’s beverage business confirmed?

No, it has not been confirmed yet. The company is exploring various options to enhance business competitiveness and efficiency, and the sale is one of the options being considered.

What are LG H&H’s main business segments?

LG H&H operates three main business segments: Beauty, HDB (Home Care & Daily Beauty), and Refreshment.

What are the key factors to consider when investing in LG H&H?

Investors should consider the progress of the restructuring, the performance of the beauty and HDB businesses, and changes in the external environment.