1. What Happened?

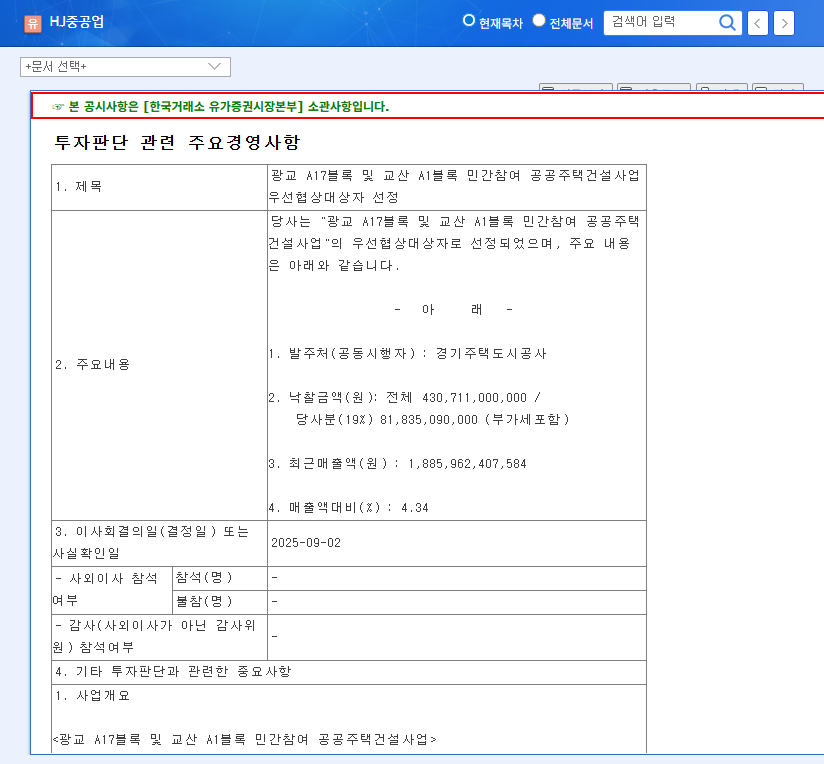

On September 2, 2025, HJ Heavy Industries was selected as the preferred bidder for the Gwanggyo A17 Block and Gyosan A1 Block public housing construction projects, ordered by Gyeonggi Housing & Urban Development Corporation. The total project size is $327 million, and HJ Heavy Industries’ stake is 19%, amounting to $62 million.

2. Why is it Important?

This contract is significant because it can provide a stable revenue base for HJ Heavy Industries’ construction division amid concerns about a recent construction downturn. Winning the public housing project also demonstrates HJ Heavy Industries’ competitiveness in the housing construction business and increases the likelihood of winning similar projects in the future.

- Positive Effects: Increased orders in the construction division, sales growth, enhanced business stability, demonstration of competitiveness in housing construction.

- Neutral/Considerations: Limited impact on overall sales, accounting for 4.34%; profitability of the project needs confirmation.

3. What’s Next?

The government’s policy to expand housing supply is expected to create a positive business environment for HJ Heavy Industries. However, macroeconomic uncertainties such as high interest rates and raw material price volatility still exist.

4. What Should Investors Do?

- Short-Term Investment Strategy: A cautious approach is necessary, considering HJ Heavy Industries’ financial soundness (high debt ratio) and the performance improvement of the shipbuilding division.

- Mid- to Long-Term Investment Strategy: Monitor additional order wins, profitability of construction projects, recovery of the shipbuilding division’s performance, and reduction of the debt ratio.

While this contract is a positive sign, investment decisions should be made considering the company’s fundamentals, performance of each business division, macroeconomic environment, and financial soundness.

Frequently Asked Questions

How much will this contract impact HJ Heavy Industries’ earnings?

The $62 million contract represents 4.34% of HJ Heavy Industries’ 2023 revenue, and the direct impact on short-term earnings may be limited. However, it has the potential to lead to increased orders and sales growth in the long term.

What are HJ Heavy Industries’ main businesses?

HJ Heavy Industries’ main businesses are construction and shipbuilding (defense/special vessels, new shipbuilding).

What should investors be aware of?

Investors should consider HJ Heavy Industries’ high debt ratio, the performance improvement of the shipbuilding division, and macroeconomic uncertainties.