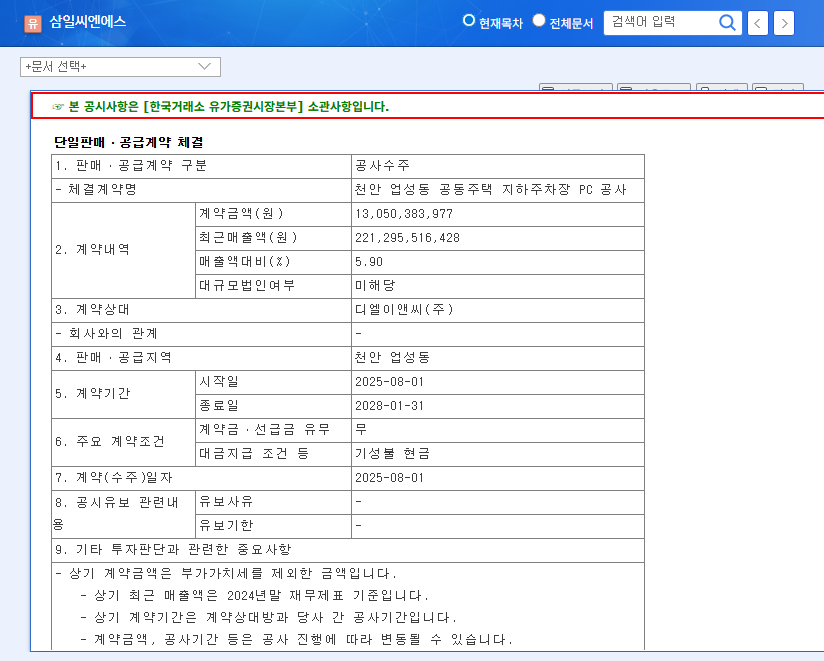

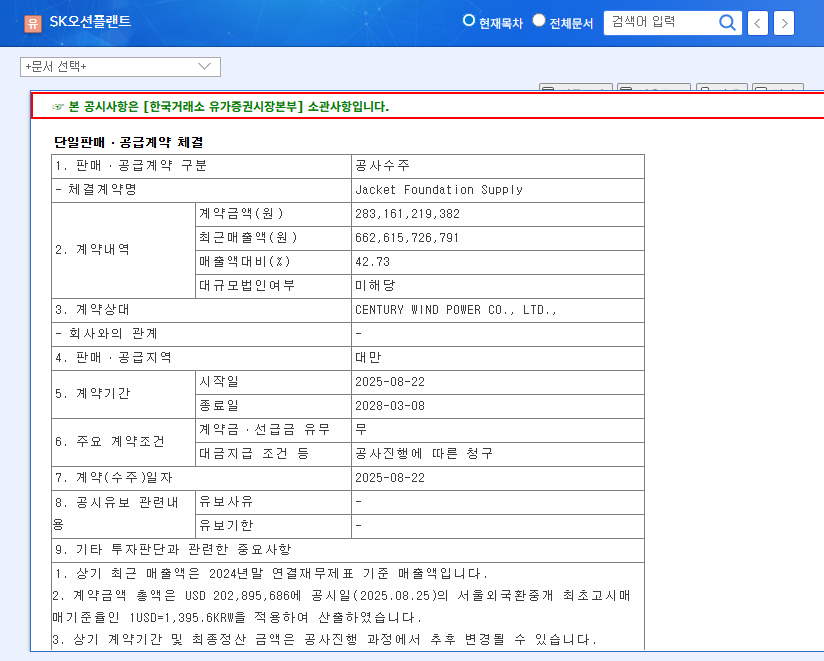

1. What’s the $89M Deal About?

Kolon Global signed an EPC (Engineering, Procurement, and Construction) contract with Yeongdeok Wind Power Co., Ltd. for the first phase of the Yeongdeok Wind Power Repowering Project. The contract is valued at KRW 118.1 billion, representing 4.05% of Kolon Global’s revenue, highlighting its commitment to expanding its renewable energy business.

2. Why is This Contract Important?

This contract is expected to positively impact Kolon Global in several ways.

- Increased Revenue and Profit: The $89 million contract will directly contribute to improved financial performance.

- Strengthened Renewable Energy Competitiveness: The experience gained in wind power EPC will serve as a valuable reference for securing similar projects in the future.

- Portfolio Diversification: Expanding into renewable energy diversifies Kolon Global’s portfolio beyond construction, enhancing stability.

While potential risks exist, such as contract duration, profit margins, and raw material price fluctuations, the South Korean government’s support for renewable energy and carbon neutrality goals further amplify Kolon Global’s growth potential.

3. What Should Investors Do?

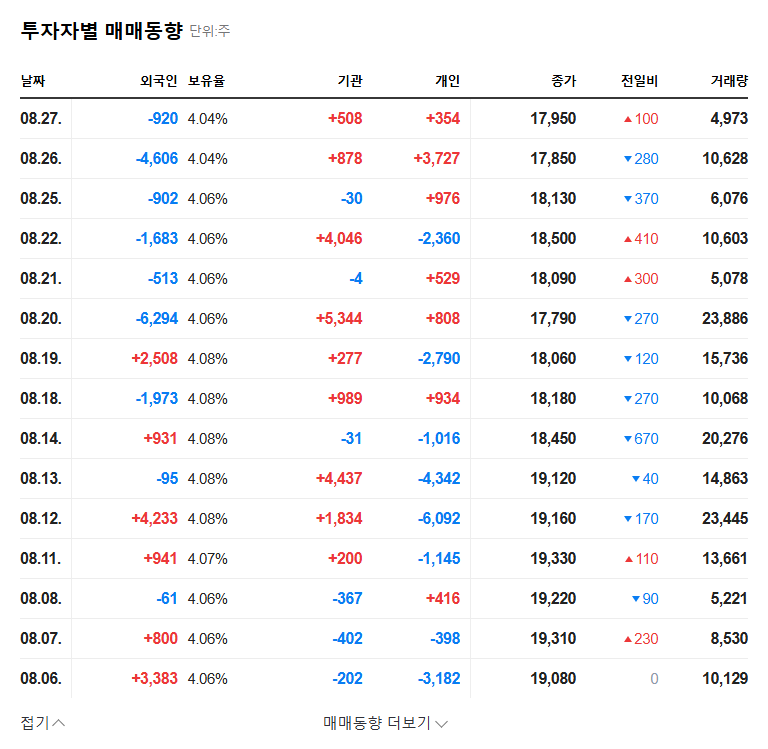

This contract could provide short-term momentum for Kolon Global’s stock price. However, a neutral approach is recommended, considering the macroeconomic environment and inherent risks in the construction industry. A comprehensive evaluation of the current stock price, future market outlook, and Kolon Global’s financial health is crucial before making any investment decisions.

Frequently Asked Questions

What is the value of this contract?

KRW 118.1 Billion, which is approximately $89 Million USD and represents 4.05% of Kolon Global’s revenue.

What are the benefits of this contract for Kolon Global?

Increased revenue and profit, strengthened renewable energy competitiveness, and portfolio diversification.

What precautions should investors take?

Carefully consider contract terms, project progress, and macroeconomic conditions.